"Japan's Economic and Freight Outlook" and "Short-term Freight Movement Survey in Japan (Nittsu Soken Tan-kan)"

August 18, 2020

Nittsu Research Institute and Consulting, lnc. (NRIC), one of the subsidiaries of Nippon Express, publishes "Japan's Economic and Freight Outlook" and "Short-term Freight Movement Survey in Japan (Nittsu Soken Tan-kan)" quarterly.

"Japan's Economic and Freight Outlook" is a survey that has continued for over 40 years since the first survey in 1974. The purpose is to investigate and analyse the trends of Japanese economy and freight transport volume of domestic freight and international freight of Japan, and to predict short-term trends of six months to one year ahead. While many research institutes carry out economic forecasts, there is no other institution that makes full-scale forecasts of Japanese freight transport.

"Short-term Freight Movement Survey in Japan (Nittsu Soken Tan-kan)" conducted the first survey in October 1988 with the aim of grasping the latest trends in corporate logistics, and since then has continued at a pace of twice a year (1st half and 2nd half). Since 2002, it has been conducted quarterly.

The survey covers 2,500 major manufacturing and wholesale business establishments in Japan. Respondents are asked to select from the three options of "increase", "stay flat", "decrease" for the actual results (expected) for the current period and the forecast for the next period for 6 items (domestic shipment volume, transport mode, import/export freight volume, inventory, freight charges and distribution cost ratio). Then, the number of responding companies for each option is aggregated for each survey item, and the ratio to the total number of companies is calculated and presented as a trend judgment index. In the June 2020 survey, we received responses from 874 companies and the response rate was 35.0%.

Summary of the results of "Japan's Economic and Freight Outlook for FY2020" (published on 17th July 2020)

●Economy

Global economy will shrink by 4.9% in 2020 due to the COVID-19 pandemic (IMF forecast). The Japanese economy is heavily damaged by the consumption tax hike in October 2019 as well as the Corona Shock. The real economic growth rate in FY2020* is estimated to be 5.6% decrease in Japan, which is much lower than that of the Lehman Brothers crisis in FY2008 with 3.4% decrease.

In Japan the government's financial year is from 1 April to 31 March.

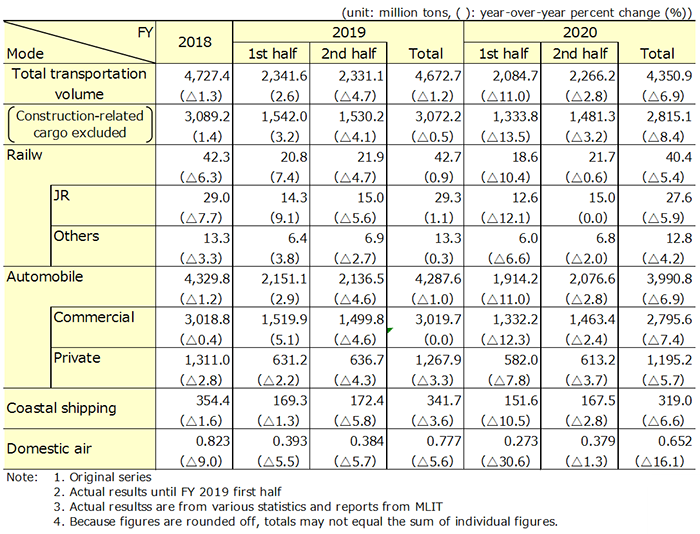

●Domestic freight transport of Japan

Due to the Corona shock, the total domestic freight volume in FY2020 is expected to decrease by 6.9% to a large negative. The growth rate is expected to be below the FY2009 level (6.0% decrease), which fell sharply due to the Lehman Brothers crisis. Consumption-related cargo and production-related cargo fell sharply, -7.4% and -9.2%, respectively, due to sluggish exports in addition to the collapse of private demand such as personal consumption and capital investment. Construction-related cargo has also fallen to -4.0% due to a significant decrease in housing investment.

Rail freight

Freight transport by JR (Japan Railway) container in FY2020 is expected to be stagnant again and decreased by 6.3%. The freight volume for most items fell below the previous year's levels due to the economic deterioration caused by the Corona Shock. Temporary relief from the shortage of truck drivers is also a negative factor for railway freight transport.

Wagonload freight is estimated to decrease by 5.0% in FY2020, a negative figure for the third consecutive year. Significant decline in FY2020 is caused by continued decrease in oil demand. In the first half of the year, demand for petroleum products was inevitably reduced due to self-restraint from going out after the Japanese government's declaration of the state of emergency. In the second half of the year, a slight decrease is expected as a reaction of the decrease in the previous year.

Truck freight

Due to diminished consumption of all commodities in FY2020, the transport volume by commercial trucks is expected to decrease by 7.4%, a minus for the first time in two years. Although special demand is expected for some home appliances such as personal computers and air conditioners, the volume of consumption-related cargo will fall due to factors such as self-restraint from going out. On the other hand, sales of general machinery, automobiles/automobile parts, steel, chemical products, etc. will be sluggish, to the minus for the first time in 5 years. Construction-related cargo will be weak due to a significant decrease in housing investment.

Freight transport by private trucks is expected to remain inactive with 5.7% decrease in FY2020. In FY2020, consumption-related and production-related cargo will decrease significantly. Although public investment is solid, housing-related investment is weak, therefore construction-related cargo will decrease slightly.

Coastal shipping freight

Freight transport by coastal shipping is expected to decline further by 6.6% in FY2020. Both production-related cargo and construction-related cargo are expected to be sluggish in FY2020, for a total of seven consecutive years of decrease.

Due to self-restraint in economic activities, demand for petroleum products will fall significantly and thus production-related cargo will inevitably expand its negative range in FY2020. Steel and chemical products are expected to be weak due to the downstream demand decline.

Construction-related cargo will drop to less than 6% in FY2020. The execution of large-scale public civil engineering works cannot be expected, and a decrease is expected especially in cement, gravel, and sand.

Domestic airfreight

In FY2020, suspensions and reductions in flights have occurred one after another, resulting in a significant reduction in domestic airfreight. In April and May 2020, the volume of airfreight was halved because of self-restraint from going out due to the Corona shock. It seems hard to break out of the shrink in demand within the year. Positive reversal will be expected from January to March 2021.

Table1: Outlook for domestic freight transport of Japan

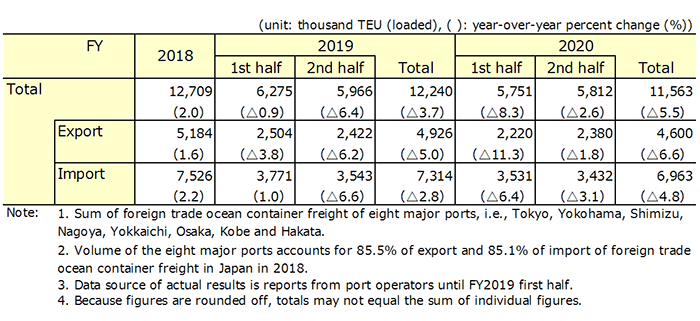

●International freight transport from/to Japan

Foreign trade ocean container freight

Exports by foreign trade ocean containers in FY2020 are expected to decline by 6.6% for the second consecutive year of decline. As the growth of the COVID-19 declines and economic activities resumes with economic measures of each country, the slowdown in the global economy growth will subside in the second half of the year, but negative growth for the second consecutive year will be inevitable. By commodity, the momentum of overseas capital investment demand recovery is weak, and industrial machinery, machine tools, and other machinery continue to show sluggish cargo movements. Delays in the recovery of production at overseas factories are another factor in pushing down the growth. With regard to automobile parts, although it is expected that they will be supported by medium to long-term demand related to EV (electric vehicle) shift and electrical equipment, the global automobile market remains stagnant, and recovery within the fiscal year cannot be expected. There is a possibility that the recovery will be delayed, and the negative range will further expand due to the US-China trade friction and second COVID-19 outbreak, etc.).

Imports by foreign trade containers in FY2020 are expected to fall by 4.8%. Regarding consumer goods such as food and clothing, slack cargo movements continues due to low personal consumption. In the first half of the year, a decline is inevitable due to the reactionary decrease in demand before the consumption tax hike in 2019. As for production goods, capital investment will continue to fall below the previous year's level, and shipments of production parts and materials and machinery will stagnate. There are also downward pressures due to the return of production bases to Japan and increased domestic procurement of parts and materials. The import of both production and consumer goods will remain sluggish throughout the year.

Table2: Outlook for foreign trade ocean container freight of Japan

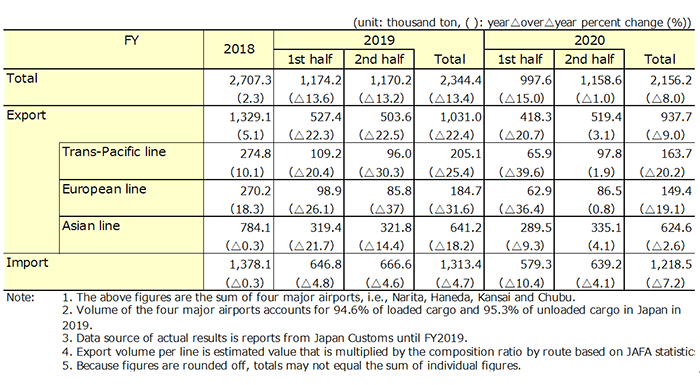

International airfreight

Exports by international air transport in FY 2020 are expected to decline by 9.0%. The mainstay Asian line is recovering clearly due to the early settling down of COVID-19. The Pacific and European lines are greatly affected by the Corona shock and lack the recovery momentum compared to the Asian line. As for semiconductor-related cargo (electronic parts and manufacturing equipment), the full-scale recovery of cargo movements will be expected due to the increased demand for AI, IoT, and 5G. Regarding automobile parts, demand for EV shifts and electrification will increase, but recovery within the year seems uncertain. As for general machinery and mechanical parts, overseas capital investment demand is slow to recover, expectations are low. In the second half of the year, although economic recovery, passenger flight recovery in each country, and a reactionary increase from the Corona shock are expected, the negative figures in the first half cannot be compensated. The level for the entire year falls below the previous year's level. There is a possibility that the recovery will be delayed, and the negative range will further expand due to the US-China trade friction and second COVID-19 outbreak, etc.

Imports by international air transport in FY2020 are expected to fall by 7.2%. Regarding consumer goods, stagnant cargo movements will continue as personal consumption continue to fall below the previous year's level. Despite the reduction of import tariffs following the trade agreement, import volume increase from point return campaign of cashless payment and 100,000 yen benefit from the government is not much expected. With regard to production goods, the recovery in business fixed investment, mainly of export companies, has slowed, and is below the level of the previous year. The return to domestic production bases to mitigate the dependence on China, and the increase in domestic procurement of parts and materials are also factors that are pushing down the growth of import by air.

Table3: Outlook for international airfreight of Japan

Read full report of "Japan's Economic and Freight Outlook" (Japanese only)

https://www.nittsu-soken.co.jp/wp-content/uploads/2020/07/report-2020717.pdf

Summary of the results of "Short-term Freight Movement Survey in Japan (Nittsu Soken Tan-kan)" (June 2020 survey, published on 4th August 2020)

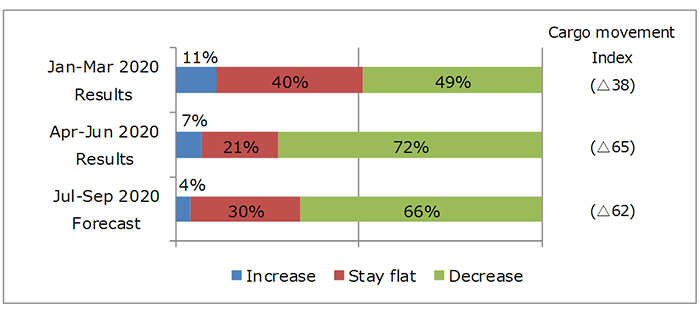

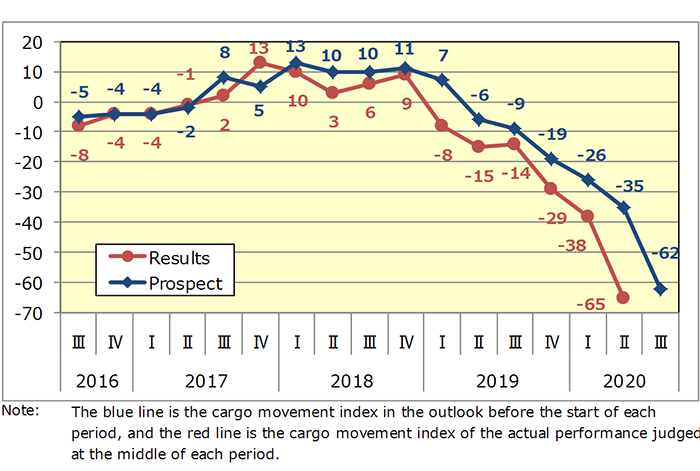

●Trends in domestic shipment volume (cargo movement index)

The "cargo movement index" in the April-June 2020 results (expected) dropped significantly to minus 65, reaching the lowest level since January-March 2009 (-75) just after the Lehman Brothers crisis. The index decreased by 27 points from the previous term (January-March 2020). The index for the July-September 2020 forecast is minus 62, increased by 3 points from the previous term (April-June 2020).

Graph1: Results and prospects for domestic shipment volume

●Changes in the "Cargo Movement Index" (2016-2020)

Since July-September 2016, the cargo movement index has started to gradually increase, and in July-September 2017, it became positive for the first time in 14 years. In October-December 2017, the result was an even higher increase.

After falling in January-March 2018 and April-June 2018, the index increased again in July-September 2018 and October-December 2018, indicating a "business peak".

A sharp decrease of 17 points in the January-March 2019 results and 7 points in the April-June 2019 results suggest a deterioration in the economy. Although it recovered 1 point in the July-September 2019 results, it decreased again in the October-December 2019 results due to the effect of the consumption tax hike, and further decreased in the January-March 2020 results.

In the April-June 2020 results, the impact of the Corona shock was severely affected, resulting in a significant decline in the index. It was the lowest level after January-March 2009 (-75) after the Lehman Brothers crisis.

Graph2: Changes in the "Cargo Movement Index" (2016-2020)

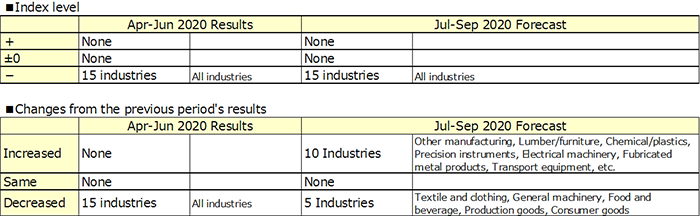

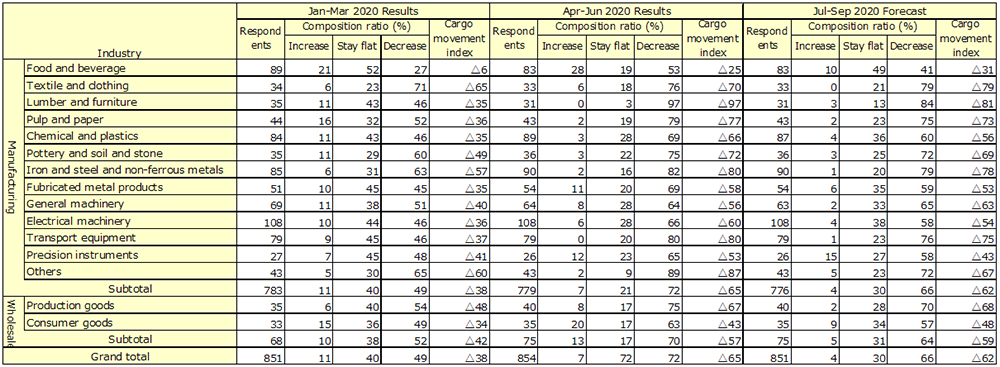

● "Cargo movement index" by industry (15 industries)

The domestic shipment volume by industry was negative for all 15 industries in the April-June 2020 results (expected) and the July-September 2020 outlook. The minus was smallest in the food and beverage manufacturing industry, which was -25 in the April-June results and -31 in the July-September outlook. In particular, 28% of respondents answered "increase" in April-June results, which shows a demand increase for food beverage even in the midst of the COVID-19 outbreak. The largest negative figure was in the lumber and furniture manufacturing industry, which was -97 in the April-June results (expected) and -81 in the July-September outlook.

The outlook for July-September 2020 is expected to be negative in all industries, but compared to the actual results in April-June, the negative range is improved in 10 industries such as other manufacturing, lumber/furniture, and chemical/plastics, etc.

Graph3: Cargo movement index by industry

Table4: Results and prospects for domestic shipment volume by industry

Read full report of "Short-term Freight Movement Survey in Japan (Nittsu Soken Tan-kan)" (Japanese only)

https://www.nittsu-soken.co.jp/wp-content/uploads/2020/08/tankan2020-6_2.pdf

Reference:

- Nittsu Research Institute and Consulting, lnc., "Japan's Economic and Freight Outlook" (Japanese only)

https://www.nittsu-soken.co.jp/wp-content/uploads/2020/07/report-2020717.pdf - Nittsu Research Institute and Consulting, lnc., "Short-term Freight Movement Survey in Japan (Nittsu Soken Tan-kan)" (Japanese only)

https://www.nittsu-soken.co.jp/wp-content/uploads/2020/08/tankan2020-6_2.pdf