"Japan's Economic and Freight Outlook" and "Short-term Survey of Freight Movement in Japan (Nittsu Soken Tan-kan)"

November 25, 2020

Nittsu Research Institute and Consulting, lnc. (NRIC), one of the subsidiaries of Nippon Express, publishes "Japan's Economic and Freight Outlook" and "Short-term Survey of Freight Movement in Japan (Nittsu Soken Tan-kan)" quarterly. For more historical details of the surveys, kindly refer to the last paragraph of this article.

Summary of the results of "Japan's Economic and Freight Outlook for FY2020" (published on 6th October 2020)

●Economy

The Global economy is projected to shrink by 4.9% in 2020 mainly due to the COVID-19 pandemic (IMF forecast). The Japanese economy has been heavily damaged by the consumption tax hike in October 2019 as well as the COVID-19 crisis. The real economic growth rate in FY2020* is estimated to be 6.0% decrease in Japan, which is much lower than that of the Lehman Brothers crisis in FY2008 with 3.4% decrease.

In Japan, the government's financial year is from 1st April to 31th March.

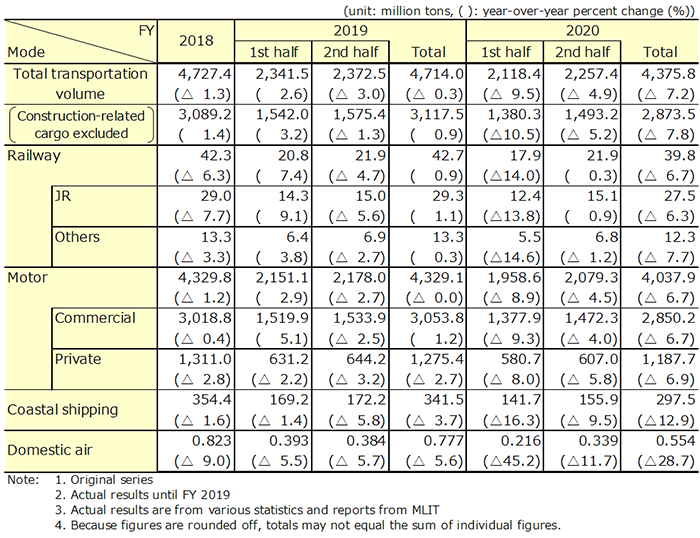

●Domestic freight transport of Japan

Due to the COVID-19 crisis and the consumption tax hike, the total domestic freight volume in FY2020 is expected to decrease by 7.2% to a large negative. The growth rate is expected to be below the FY2009 level (6.0% decrease), which fell sharply due to the Lehman Brothers crisis.

Due to sluggish private demand such as personal consumption, capital investment and stagnant exports, production-related freight is projected to be significantly negative by 9.5% in FY2020. Consumption-related freight is also expected to decrease by 5.6%. While public investment is positive, construction-related freight is also expected to be negative by 5.9% due to a significant decrease in housing investment.

Rail freight

Rail freight transport is expected to decrease by 6.7% in FY2020.

Freight transport by JR (Japan Railway) container in FY2020 is expected to be stagnant again and decreased by 6.3%. The freight volume for most items fell below the previous year's levels due to the economic deterioration caused mainly by the COVID-19 crisis. Temporary relief from the shortage of truck drivers is also a negative factor for railway freight transport. JR wagonload freight is estimated to decrease by 5.4% in FY2020, a negative figure for the third consecutive year. In the first half of the year, the wagonload freight volume decreased mainly due to inevitably reduced demand for fuel oil caused by self-restraint from going out after the Japanese government's declaration of the state of emergency. In the second half of the year, a slight increase is expected as a reaction of the decrease in the previous year.

Rail freight transport other than JR is expected to fall 7.7% due to sluggish demand for oil, cement, and limestone.

Motor freight

Due to diminished consumption of all commodities in FY2020, the transport volume by commercial trucks is expected to decrease by 6.7%, a minus for the first time in two years. The volume of consumption-related freight will fall due to factors such as self-restraint from going out. With regard to production-related freight, the sales of general machinery, automobiles, machine components, steel, chemical products, etc. will be sluggish; therefore the volume of production-related freight is expected to be minus for the first time in 5 years. Construction-related freight will be weak due to a significant decrease in housing investment.

Freight transport by private trucks is expected to remain inactive with 6.9% decrease in FY2020. Although public works projects are strong, large-scale civil engineering works cannot be executed, and housing investment is sluggish, resulting in a decrease in construction-related freight. Consumption-related freight and production-related freight are forecast to decrease by double digits.

Coastal shipping freight

Freight transport by coastal shipping is also projected to be stagnant for both production-related freight and construction-related freight, such as a significant decrease in petroleum products, steel, and chemical products, which occupy a large weight, and the total will decrease by 12.9% for the seventh consecutive year.

Domestic airfreight

Domestic airfreight is expected to decrease sharply by 28.7% due to low demand and a decline in supply capacity of aircrafts caused by the self-restraint from going out due to the COVID-19 crisis. In the April-June period, the airfreight volume was halved because of the decline in supply capacity. It seems hard to break out of the shrink in demand within FY2020.

Table1: Outlook for domestic freight transport of Japan

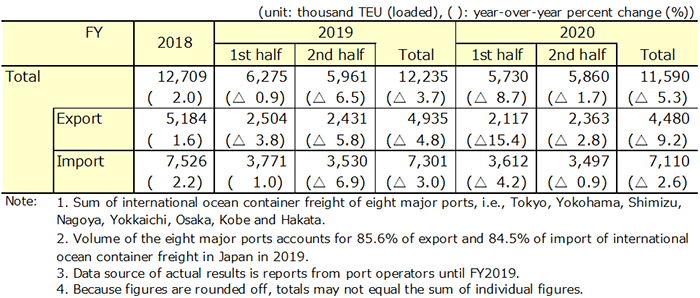

●International freight transport from/to Japan

International ocean container freight

Exports by international ocean containers are expected to decrease by 9.2% in FY2020. In the April-June period, the negative range increased significantly from the previous period due to the downward pressure caused mainly by the COVID-19 crisis. Although sales to China have improved slightly, sales to Europe and the United States have decreased significantly by 30-40%. The slowdown in the world economy seems to subside in the second half due to the resumption of economic activities and economic measures in each country, though the pace of recovery will be slow due to the effects of the re-spread of infection. A negative growth for the second consecutive year is inevitable, and the rate of decrease is expanding. The recovery of overseas capital investment demand is weak, and freight movements of machinery such as industrial machinery and machine tools are continuously sluggish, falling below the previous year's level. Delays in the recovery of production at overseas factories are also a factor pushing down the freight volume. There is a possibility that the negative range will further expand due to the US-China trade friction, re-emerging of COVID-19 outbreak, and delays in return of liner container freight services.

Imports by international ocean containers are expected to fall 2.6% in FY2020. In the April-June period, the rate of decrease was improved from the previous period. As for consumer goods, food products remained firm, and clothing and furniture also picked up. As for production goods, automobile parts remained stagnant, and machinery remained sluggish. As for consumer goods, the recovery momentum of individual consumption is weak, and freight movements continue to be sluggish. In the first half of the year, a decline due to a reactionary decline in demand for the tax hike in the previous year is inevitable. With regard to production goods, capital investment continued to fall below the previous year's level, and freight movements for production parts/components and machinery stagnated. In the January-March quarter, personal consumption picked up and was pushed up in reaction to the sharp decline in the previous year.

Table2: Outlook for international ocean container freight of Japan

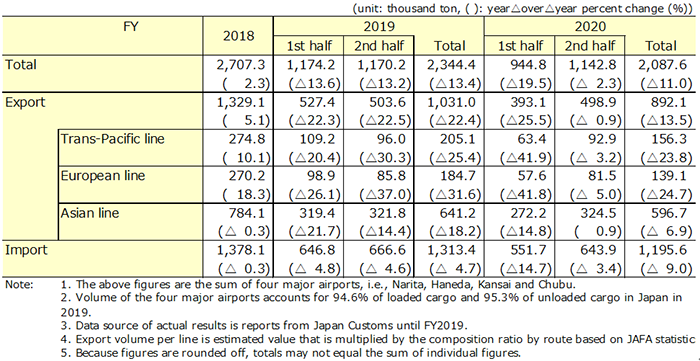

International airfreight

International airfreight exports are expected to decrease by 13.5% in FY2020. The recovery trend of Asian lines is clear due to the early settle down of the COVID-19 pandemic. On the European and Pacific lines, the downside due to the COVID-19 crisis will be prolonged because of the re-expansion of infection, and recovery will be lack of momentum. Semiconductor-related products (electronic parts / manufacturing equipment) continue to increase in response to rising demand for AI / IoT / 5G-related products. Although demand for EV shifts and electrical equipment is supporting the demand for automobile parts, recovery within FY2020 can hardly be expected. As for general machinery and mechanical parts, the recovery of overseas capital investment demand is sluggish, and freight movements continue to stagnate. In the second half, economic recovery in each country, full-scale return of passenger flights, and a reactionary increase from the COVID-19 crisis of the previous year are expected. But they would not reach the previous year's level, and the year as total is expected to fall by double digits for the second consecutive year. There is a possibility that the negative range will further expand due to the US-China trade friction, re-emerging of COVID-19 outbreak, or delays in return of regular container flights.

International airfreight imports are expected to decline by 9.0% in FY2020. The freight movement of foodstuffs stalled and decreased significantly, and the freight movement of machinery and parts, except for electronic parts and electrical machinery, was further stagnant. As individual consumption continues to fall below the previous year's level, consumer goods will continue to be sluggish in the second half. The decline in import duty rates following the trade agreements has eased the negative margin to a point. For production goods, the recovery in capital investment, mainly of export companies, has slowed, and is below the level of the previous year. The return to domestic production bases to mitigate the dependence on China, and the increase in domestic procurement of parts and materials are also factors that are pushing down the growth of import by air. In the January-March period, there will be a boost due to an increase in emergency imports of pharmaceuticals (vaccines, therapeutic agents, etc.) and medical care.

Table3: Outlook for international airfreight of Japan

Read full report of "Japan's Economic and Freight Outlook" (Japanese only)

https://www.nittsu-soken.co.jp/wp-content/uploads/2020/10/report-20201006.pdf

Summary of the results of "Short-term Freight Movement Survey in Japan (Nittsu Soken Tan-kan)" (September 2020 survey, published on 30th October 2020)

In the September 2020 survey, questionnaires are sent to 2,500 major manufacturing and wholesale business establishments in Japan and we received responses from 855 business establishments. The response rate was 34.2%.

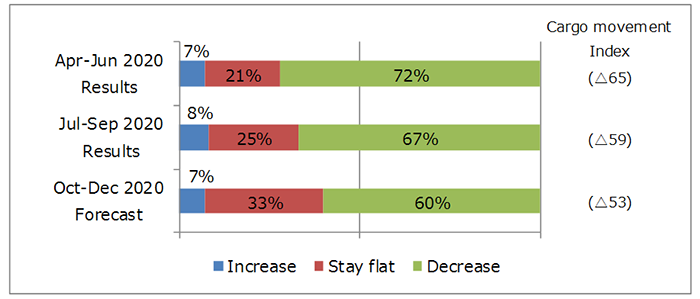

●Trends in domestic shipment volume (freight movement index)

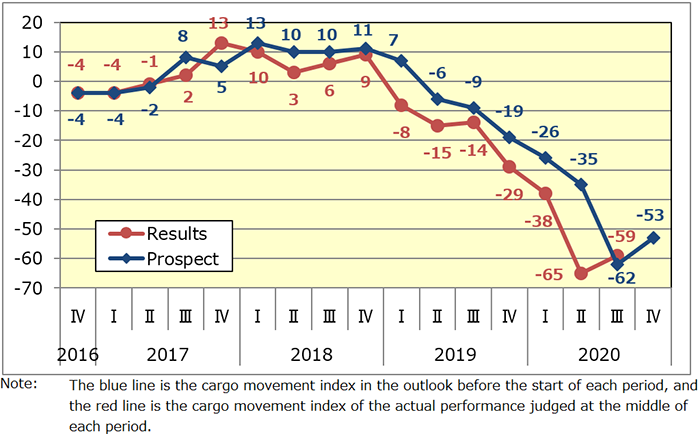

The "freight movement index" in the July-September 2020 results (expected) was minus 59, 6-point increase from the previous term (April-June 2020). The index for the October-December 2020 forecast is minus 53, increased further by 6 points from the current term (July-September 2020).

Graph1: Results and prospects for domestic shipment volume

●Changes in the "Freight Movement Index" (2016-2020)

After falling in January-March 2018 and April-June 2018, the index increased again in July-September 2018 and October-December 2018, indicating a "business peak".

A sharp decrease of 17 points in the January-March 2019 results and 7 points in the April-June 2019 results suggest a deterioration in the economy. Although it recovered 1 point in the July-September 2019 results, it decreased again in the October-December 2019 results because of the consumption tax hike, and further decreased in the January-March 2020 results.

In the April-June 2020 results, the impact of the COVID-19 crisis was severely affected, resulting in a significant decline in the index. It was the lowest level after January-March 2009 (-75) and April-June 2009 (-69) after the Lehman Brothers crisis.

The July-September 2020 results turned up. The outlook for October-December 2020 term is expected to rise further.

Graph2: Changes in the "Freight Movement Index" (2016-2020)

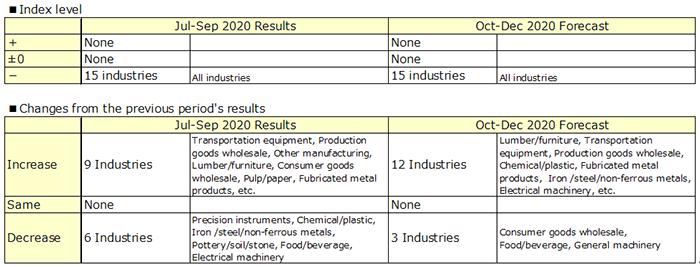

Graph3: Freight movement index by industry

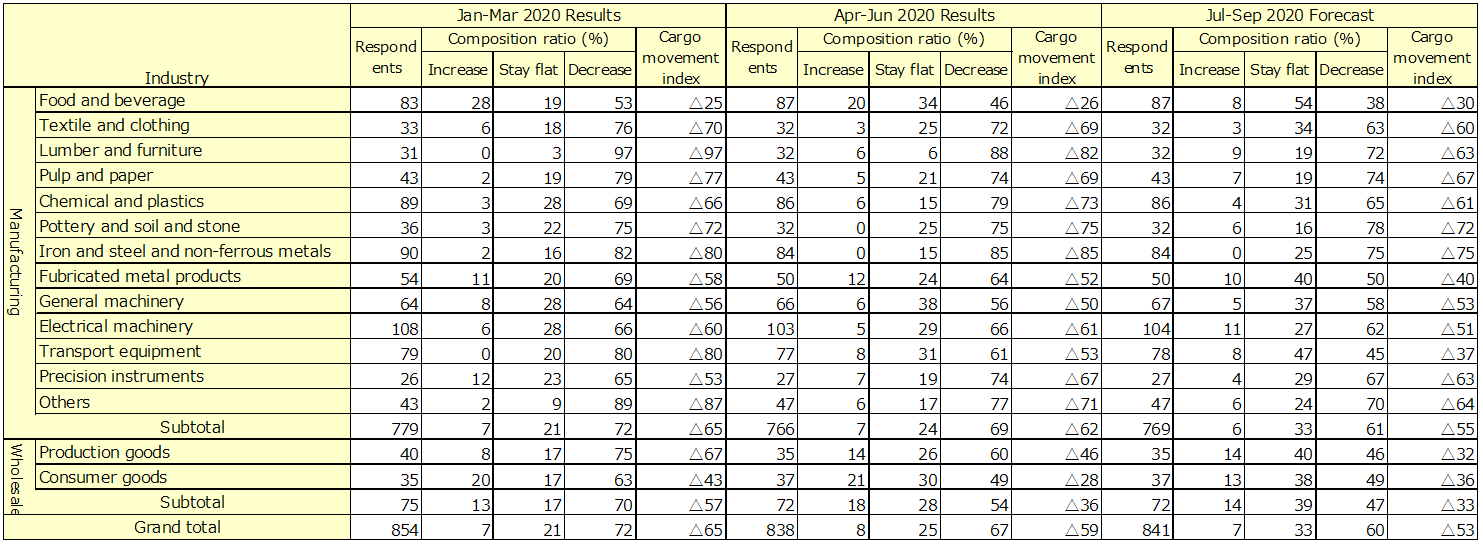

Table4: Results and prospects for domestic shipment volume by industry

Read full report of "Short-term Freight Movement Survey in Japan (Nittsu Soken Tan-kan)" (Japanese only)

https://www.nittsu-soken.co.jp/wp-content/uploads/2020/10/tankan2020-10.pdf

"Japan's Economic and Freight Outlook" is a survey that has continued for over 40 years since the first survey in 1974. The purpose is to investigate and analyse the trends of Japanese economy and freight transport volume of domestic freight and international freight of Japan, and to predict short-term trends of six months to one year ahead. While many research institutes carry out economic forecasts, there is no other institution that makes full-scale forecasts of Japanese freight transport.

"Short-term Survey of Freight Movement in Japan (Nittsu Soken Tan-kan)" is one and only diffusion index survey on freight movements in Japan. Its first survey was conducted in October 1988 with the aim of grasping the latest trends in corporate logistics. Since then, it has continued at a pace of twice a year (1st half and 2nd half) and since 2002, it has been conducted quarterly.

Questionnaires are sent to 2,500 major manufacturing and wholesale business establishments in Japan and the response rate is approximately 30-40%. Respondents are asked to select from the three options of "increase", "stay flat", "decrease" for the actual results (expected) for the current period and the forecast for the next period for 6 items (domestic shipment volume, transport mode, import/export freight volume, inventory, freight charges and distribution cost ratio). Then, the number of responding companies for each option is aggregated for each survey item, and the ratio to the total number of business establishments is calculated and presented as a trend judgment index.

Reference:

- Nittsu Research Institute and Consulting, lnc., "Japan's Economic and Freight Outlook" (Japanese only)

https://www.nittsu-soken.co.jp/wp-content/uploads/2020/10/report-20201006.pdf - Nittsu Research Institute and Consulting, lnc., "Short-term Survey of Freight Movement in Japan (Nittsu Soken Tan-kan)" (Japanese only)

https://www.nittsu-soken.co.jp/wp-content/uploads/2020/10/tankan2020-10.pdf